A lot has been made of the recent spike in the VIX, which in February jumped from single-digit levels to nearly 50% following a prolonged period of low volatility. Now that “volatility is back”, we thought it would be a good time to examine what exactly the VIX measures are and how to interpret them.

Implied volatility

Implied volatility, the heart of the VIX, is often described as an

ex-ante (forward-looking) measure of risk precisely because it does not rely on historical data. Before the advent of the Black-Scholes pricing formula, volatility was only measured using historical returns. Historical volatilities measure market price movements that already happened rather than anticipating what volatilities may lie ahead. Measuring historical volatility provides a number that represents the middle of the historical window: a 60-day volatility is correct, on average, about 30 days ago. It leaves completely unanswered the question of current market volatility. These ex-post volatility measures are appropriate for understanding historical dynamics but are less suitable for forward-looking purposes like hedging or asset allocation.

The VIX was introduced to provide a forward-looking estimate of equity volatility. The Black-Scholes model, used in the traditional way, provides an estimate of the fair-market price for options based on a number of inputs including the SPX ex-post volatility computed from historical prices. The formula can be used “backwards” – instead of computing the price of the option using the volatility, you can use the market price of the option to compute the volatility that matches the observed market price. That volatility is “implied” by the model: it’s the only volatility consistent with the market-observed prices. In this way, the VIX is calculated using information about current market conditions.

The VIX itself is computed from SPX call and put options expiring about 30 days ahead, and so represents the current market’s best guess of what the volatility will be in 30 days. It is “forward-looking” in that we assume market participants have priced short-term options consistent with an expectation that the future volatility will be the value implied through the Black-Scholes equation.

How forward-looking is it, really?

Consider for a moment the case of equities pricing via the discounted cash flow analysis method: a case can be made that a stock’s price is simply the market’s reflection of the discounted expected future cash flows. However, the computation relies on predictions about uncertain future cash flows and a discount rate to calculate their net present value. Real-life divergences from assumptions underpinning the analysis cause equity prices that can be quite different from what we calculate. In addition, the cash flows themselves do not depend on the implied stock price. It is in the same way that future volatility is not dependent on the market’s implied volatility.

VIX’s prediction of volatility

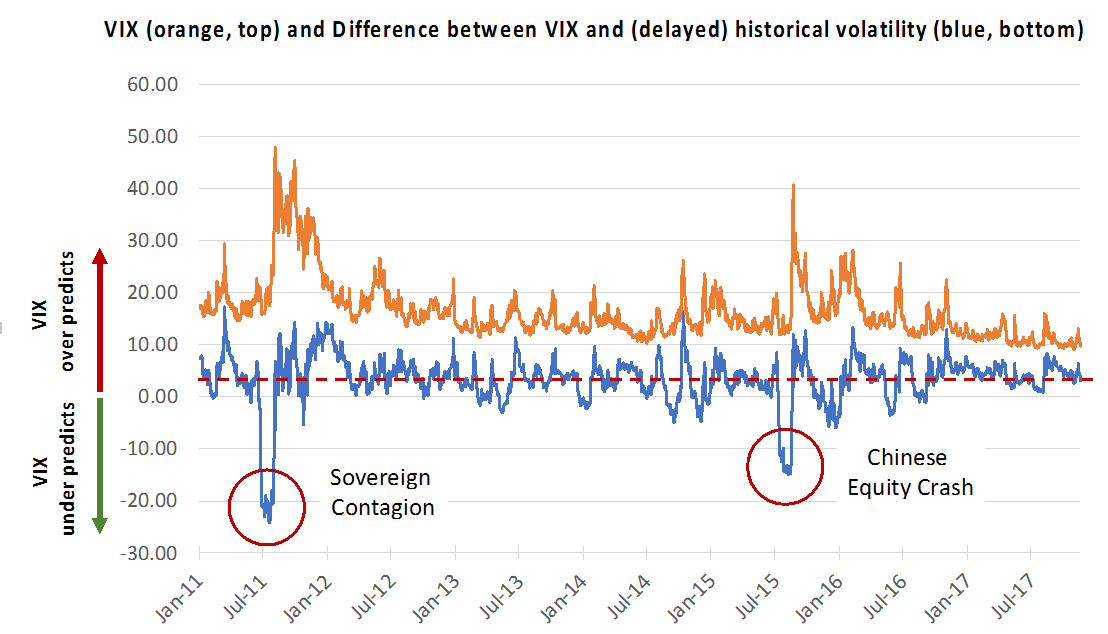

To probe this a bit more deeply, we looked at how closely the VIX’s predictions of volatility match the realized historical volatility 30 days later. Figure 1 shows the spread between the VIX and the rolling daily 30-day historical volatility of the S&P delayed by 30 days over a

six-year period. The delay is used to compare the VIX on a given day with the volatility that was subsequently experienced over the next 30 day period. Positive values of the spread correspond to VIX over predicting realized volatility and negative values correspond to VIX under predicting the realized volatility.

The average spread during the period from January 2011 to November 2017, shown in the horizontal red line, is 3.3 points over an average VIX value of 16. In other words, the VIX systematically over predicted the SPX volatility by about three points, or 20% of the VIX’s average value. Measured this way, the VIX does a good job overall of identifying the forward-looking volatility – for most markets.

Episodes of market crisis, when knowledge of the forward volatility is most valuable, are a different story. There are two periods highlighted in Figure 1 when the spread spiked down – times when the VIX under-predicted the real market volatility – by 15% or more. The periods in 2011 and 2015 correspond to the sovereign debt contagion scare of 2011 and the Chinese equity crash of 2015. It seems the VIX functions worst precisely when it’s needed most.

Figure 1: Orange line (top) is the VIX. Blue line (bottom) is the spread between the VIX and the (appropriately delayed) historical volatility. The dashed red line is the average of the spread over the entire period, 3.3 points. During this period, the VIX average value was 16%.

In both highlighted cases, the VIX under-predicted actual volatility in that its value, 30-days prior to a market sell-off, was far below what was experienced over the next month. However, the VIX rose dramatically as soon as markets began selling off and doing so much faster compared to historical volatility. This should not be surprising: the VIX is computed from options market prices. For this reason, a spike in VIX can only come from information that has made its way into the options markets. Despite its reputation as a “forward-looking” volatility measure, the VIX is, of course, incapable of predicting market crashes. Rather than thinking of it as a predictor of risk, the VIX should be thought of as a “rapidly responding” volatility indicator. It is not quite a leading indicator, but more akin to a real-time indicator.

The market sell-off and VIX spike of 6 February 2018 from single-digits to about 50 is analogous to the sovereign debt contagion scare and Chinese equity crash events: the VIX responded to the equity markets’ sell-off in a matter of minutes while historical volatility took days to reflect the increase in market volatility.

VIX is not a crystal ball

The lesson for market participants is that the VIX, like any measure based on market prices, is not a crystal ball. Rather, it is more sensitive to equity movement and responds faster than any other estimate of volatility. During normal markets, it provides a reasonably accurate estimate of risk, with an average bias of about three points. During times of stress, the VIX is a rapid-response analytic. While it cannot give advance warning of market downturns, it can and does provide a fast-acting alarm that markets are riskier than they were in the recent past.

Many StatPro clients use the VIX and other volatility-based indices as part of a multi-factor approach to risk management. These clients use our Revolution Risk modules to stress volatility indices like the VIX to observe how other market drivers would respond, and then apply those stresses to their own portfolios. Stress testing using the VIX helps market participants estimate the impact of dynamic shocks to volatility on their portfolios.

{{cta(‘f543e487-b4d2-495c-a07a-cfa4a233f17e’)}}