The long is even longer

The U.S. government bond market, a cornerstone of the global financial system, is the world’s largest and most actively traded. As Scott Bessent steps into the role of Treasury Secretary in the US, he faces the colossal task of managing the issuance of trillions of dollars in government bonds. Among his strategies is introducing ultra-long-term bonds (50- to 100-year Treasuries), an idea previously explored by Steven Mnuchin, who served as the 77th United States Secretary of the Treasury from 2017 to 2021, during the administration of President Donald Trump. This approach reflects confidence in stable interest rates and marks a potentially transformative strategy for managing the $36 trillion U.S. debt.

Ultra-long bonds: Purpose and demand

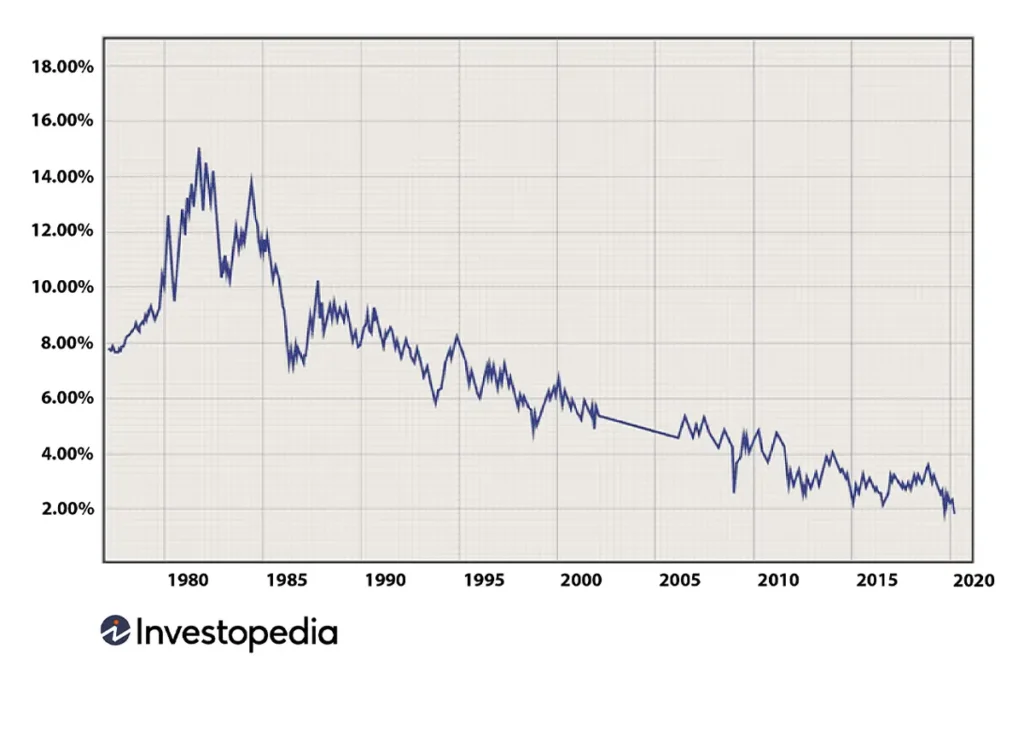

Ultra-long bonds provide a clear signal of how the US Treasury plans to manage its debt amidst shifting economic conditions. If sufficient demand exists, these bonds aim to reduce the risk associated with accumulated debt by locking in low interest rates for an extended period. Pension funds and insurance companies, with their long-term liabilities, are primary investors in these bonds, although they typically do not hold them to maturity. Currently, the longest-dated U.S. Treasury is a 30-year bond maturing in 2054, offering a 4.50% yield.

Globally, countries like Canada, Ireland, and Mexico have already issued 50- and 100-year bonds. China’s recent allocation of $139.5 billion in ultra-long special government bonds to stimulate trade and infrastructure development demonstrates the growing appeal of these instruments in addressing macroeconomic challenges.

Key benefits

- Security: Treasury bonds are considered the most secure in the market, making them easy to buy and sell.

- Accessibility: Investors can purchase long bonds directly from the government or through mutual funds.

- Stabilizing Infrastructure Financing: Century bonds can fund long-term projects like bridges and airports, reducing reliance on short-term debt and easing taxpayer burdens.

Challenges to consider

- Interest Rate Sensitivity: Long bonds are more sensitive to interest rate changes, with prices falling sharply if rates rise.

- Inflation Risk: Inflation erodes the purchasing power of bond returns, particularly over longer terms.

- Liquidity Concerns: Ultra-long bonds have lower liquidity due to limited demand in this niche market.

While investors in long bonds typically receive higher yields to compensate for longevity risks, Treasury Inflation-Protected Securities (TIPS) offer an alternative for those concerned about inflation.

Historical context and future outlook

The concept of ultra-long bonds is not new; the Treasury has revisited the idea several times over the past decade. Long-term Treasuries have proven resilient during financial crises, such as Black Monday (1987), the Lehman Brothers collapse (2008), and the COVID-19 pandemic (2020). These bonds remain attractive during periods of market volatility and economic uncertainty.

Source: Investopedia

The introduction of ultra-long bonds will reshape yield curve strategies, encouraging asset managers to adopt innovative approaches to duration and inflation risks. Growth-oriented policies under the new U.S. administration, including tax reforms and infrastructure spending, may elevate inflationary pressures, necessitating agile portfolio adjustments. Financing long-term projects with short-term debt can create financial strain, making ultra-long bonds a better choice for sustainable fiscal management.

Bessent’s commitment to preserving the U.S. dollar’s status as the world’s reserve currency ensures continued demand for Treasuries, solidifying their role as a strategic asset for global investors. As the U.S. embarks on ambitious billion-dollar infrastructure projects, ultra-long bonds will likely become a pivotal financing tool, offering asset managers an avenue for stable, long-duration investments.

On the downside, long-term bond yields tend to be relatively low compared to corporate long bonds. Inflation risk—when inflation rises, the purchasing power of bond returns decreases, especially for longer-term bonds. Treasury Inflation-Protected Securities (TIPS) are bonds that adjust for inflation. Very few investors put their money in this asset class, and these investors have many options available. Therefore, there isn’t much liquidity for these bonds.

Despite the negative feedback, the American government will likely issue them in the near future to rebuild its infrastructure. Infrastructure projects like bridges, ports, and airports take a long time to break even. If the government finances these long-term projects with short-term debt, it will find itself in a tight spot; therefore, ultra-long bonds are a better choice.

Changing yield curve

A shift in the strategy will require investors to stay agile and diversify their portfolios. Particularly for investors weighing duration against inflation risks, ultra-long bonds create new dynamics in portfolio management and steepen the yield curve. Growth-oriented policies, such as tariffs, tax breaks, and infrastructure spending, may increase inflationary pressures and make the outlook for fixed incomes more difficult.

For investors are looking for secure, long-duration assets with higher interest rates, ultra-long term bonds are the answer in a stable low inflation environment. As the financial landscape continues to evolve, ultra-long bonds stand poised to play a transformative role in shaping the future of asset management.

Evaluated bond pricing in turbulent markets

Bond valuation is a complex and dynamic process that requires accurate and timely data, especially in volatile and uncertain market conditions. Confluence’s bond valuation platform provides firms with reliable and consistent bond valuations. The valuation methodologies are based on external inputs and adjusted according to spreads and other market factors. Trust Confluence’s bond valuations and valuation methodology to reflect your bond portfolio’s true value and help you make informed investment decisions in any market scenario.

Disclaimer

The content provided by Confluence Technologies, Inc. is for general informational purposes only and does not constitute legal, regulatory, financial, investment, or other professional advice. It should not be relied upon as a substitute for specific advice tailored to particular circumstances. Recipients should seek guidance from appropriately qualified professionals before making any decisions based on this content.

Unless otherwise stated, Confluence Technologies, Inc. (or the relevant group entity) owns the copyright and all related intellectual property rights in this material, including but not limited to database rights, trademarks, registered trademarks, service marks, and logos.

No part of this content may be adapted, modified, reproduced, republished, uploaded, posted, broadcast, or transmitted to third parties for commercial purposes without prior written consent.

Author

About Confluence® Technologies

Confluence is a global leader in enterprise data and software solutions for regulatory, analytics, and investor communications. Our best-of-breed solutions make it easy and fast to create, share, and operationalize mission-critical reporting and actionable insights essential to the investment management industry. Trusted for over 30 years by the largest asset service providers, asset managers, asset owners, and investment consultants worldwide, our global team of regulatory and analytics experts delivers forward-looking innovations and market-leading solutions, adding efficiency, speed, and accuracy to everything we do. Headquartered in Pittsburgh, PA, with 700+ employees across North America, the United Kingdom, Europe, South Africa, and Australia, Confluence services over 1,000 clients in more than 40 countries. For more information, visit www.confluence.com.