Q1 2026 Plan Universe Allocation & Return Analysis

Executive summary

The Q1 2026 Confluence Plan Universe Report – the industry’s most granular analytics tool for plan sponsors with data sourced directly from over 4,000 institutions – reported its first negative quarter for defined benefit plans since Q4 2024 with a median return of -.81%. The median defined benefit plan returned 11.16% for the year end March, which would trail a traditional 60/40 benchmark return by 2.76%.

After a robust start to the year, global equity markets sold off in March due to conflict in the Middle East. Foreign markets, especially emerging markets, bore the brunt of the risk-off sentiment with the MSCI Emerging Markets Index returning -13.03% in March. Concerns of inflation and slowing growth also impacted domestic equities with the Russell 1000 Index returning -4.18% and the Russell 1000 Growth Index returning -.978% for the quarter. Within fixed income, the U.S. Bloomberg Aggregate Index returned -.05% for the quarter, while the Bloomberg U.S. Long Treasury Index returned -.41%.

Highlights

- All defined benefit plans posted a median return of 11.16% for the year ending March, underperforming a traditional 60/40 benchmark return of 13.92%. (60% MSCI ACWI Index/40% Bloomberg Barclays U.S. Aggregate Index).

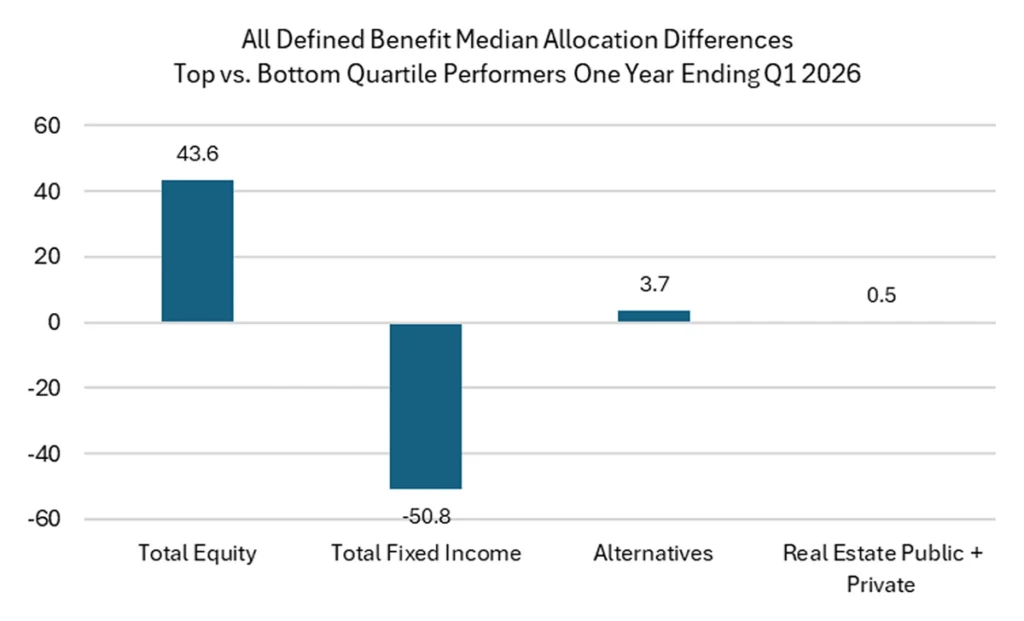

- For the year ending March, the median allocation to equity for top quartile performing plans was 59.5%, compared to 15.9% for the bottom quartile performers.

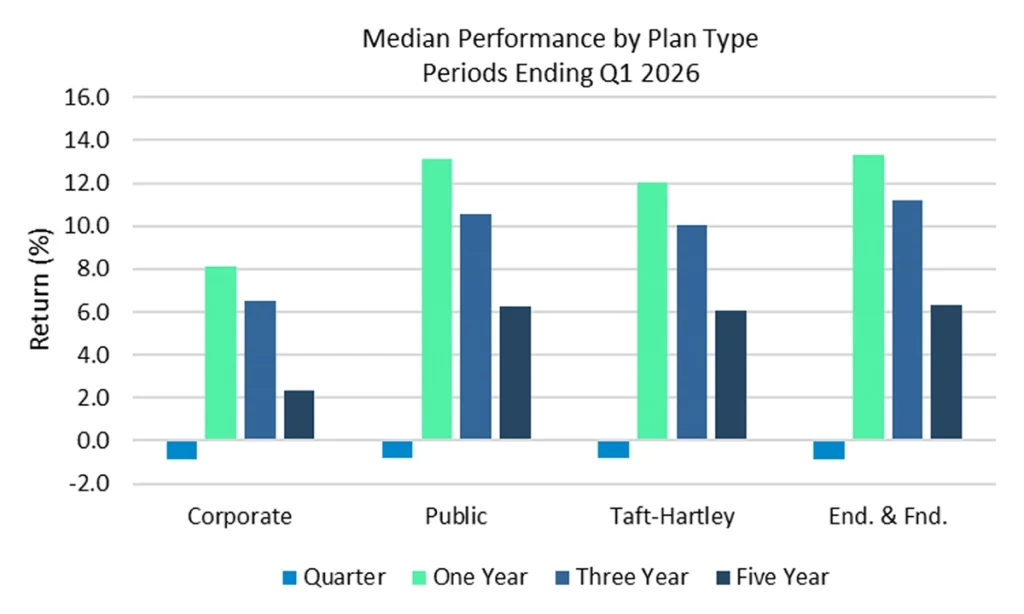

- For the one-, three-, and five-year periods ending March, Endowments & Foundations delivered the strongest performance driven by their high allocations to equity and alternative markets.

- Corporate plans, driven by their comparatively high fixed income allocations, delivered the weakest performance by plan type for the one-, three-, and five-year periods.

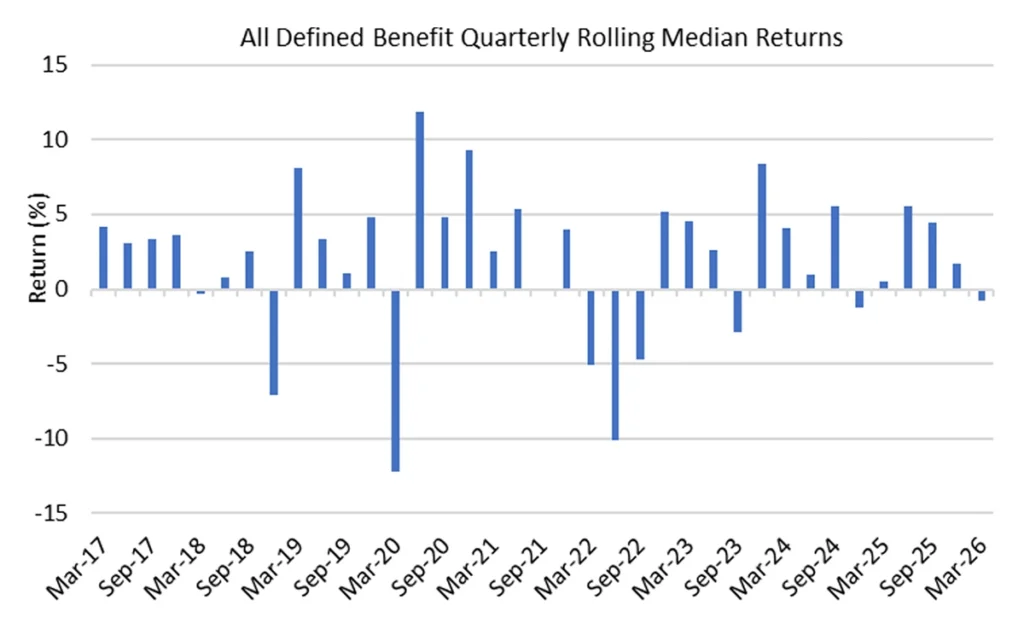

Plan performance over time

For the quarter, the Confluence All Defined Benefit Plan Sponsor Universe posted a median return of -.81%. For the year ending March, DB plans posted a median return of 11.16%, underperforming a traditional 60/40 benchmark return of 13.92%. (60% MSCI ACWI Index/40% Bloomberg Barclays U.S. Aggregate Index).

Source: Confluence

For the year, plans with a return greater than 13.42% were top quartile performers while plans returning less than 8.02% fell in the bottom quartile. The median allocation to equity for top quartile performing plans was 59.5%, compared to 15.9% for the bottom quartile. Conversely, the bottom quartile performing plans had a median allocation of 77.7% to fixed income, 50.8% higher than the top quartile allocation of 26.9%.

Source: Confluence

Historical plan comparison

Endowments & Foundations delivered the strongest performance for the year ending March, with median return of 13.31%. Corporate plans, which have significantly higher exposures to fixed income compared to other plan types, delivered the weakest performance over the one-, three-, and five-year periods.

Source: Confluence

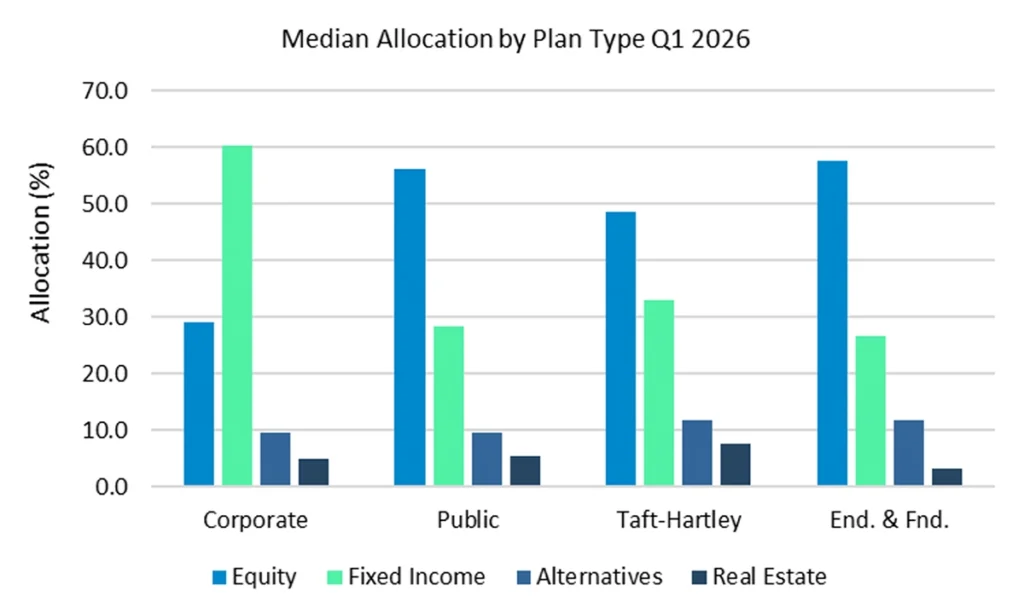

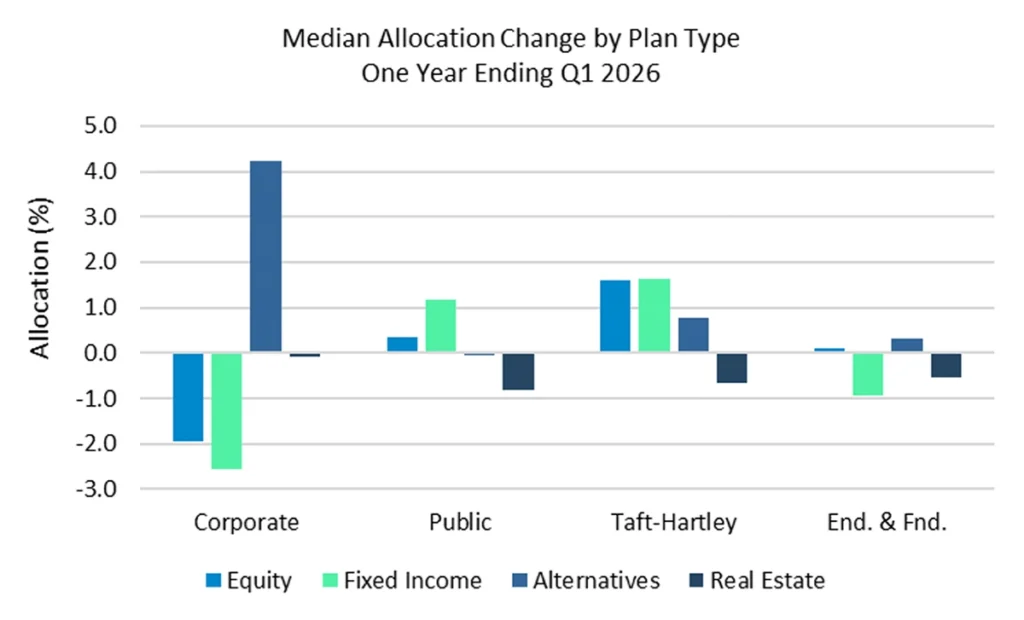

Plan allocation analysis

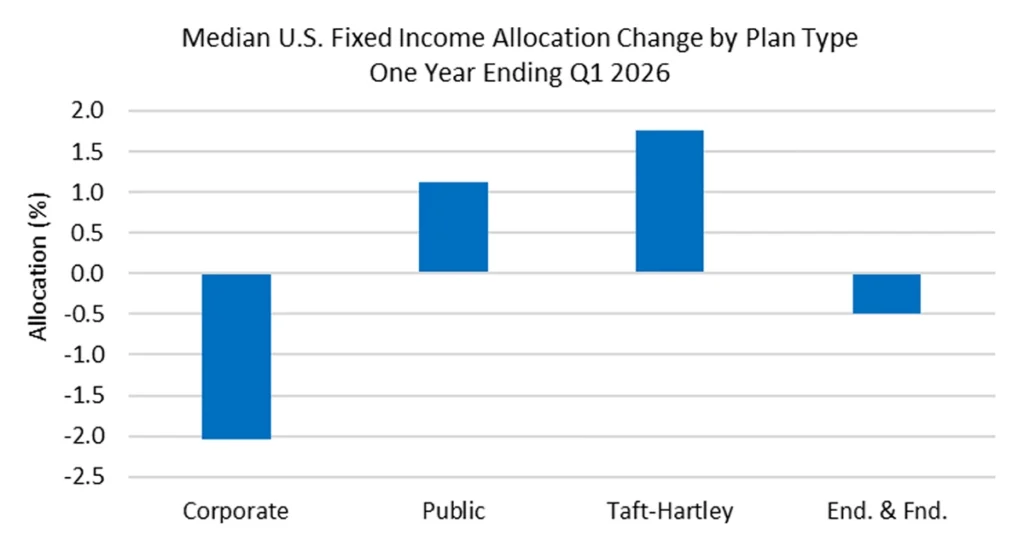

Despite some shifts in allocations, Corporate plans maintain the largest allocation to fixed income at 60.3%. The median allocations to equity, the best performing asset class, increased for Taft Hartley, Public and Endowment & Foundation plans over the last year. Allocations to Real Estate, the worst-performing asset class over the last year with a median return of 3.81%, were down across all plan types by an average of .53%.

Source: Confluence

Source: Confluence

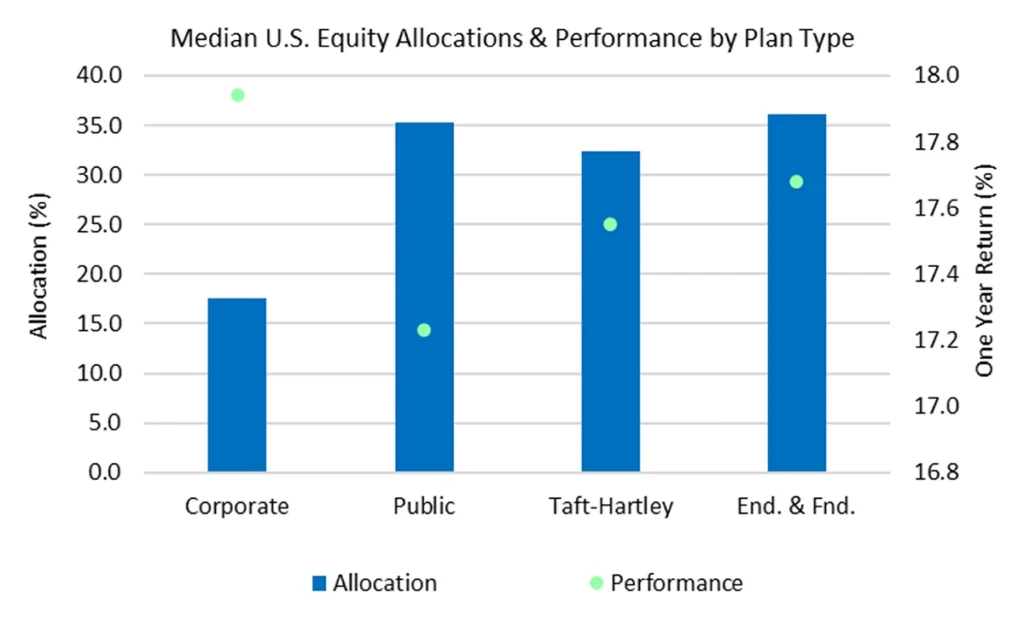

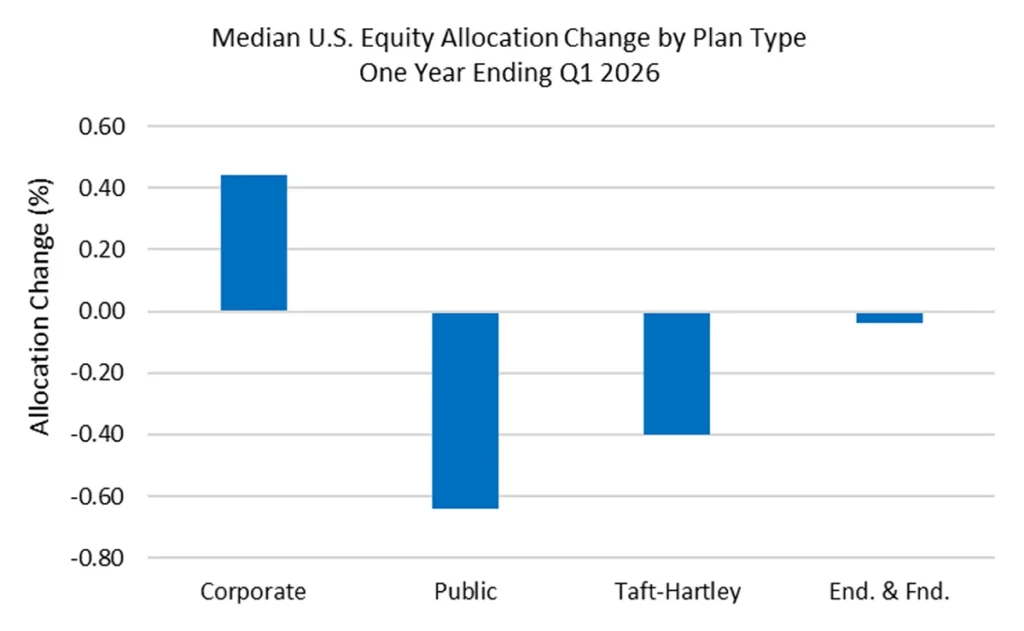

U.S. equity performance

Although U.S. public equity markets sold off during the first quarter, returns remain strong over the trailing year with the Russell 1000 Index returning 17.74%. Comparatively, the median U.S. equity return for all defined benefit plans was 17.65%. Corporate plans, the only plan type to see an increase in exposure to U.S. equity, continue to be underweight with a median allocation of 17.6%, nearly half of the allocation compared to other plan types.

Source: Confluence

Source: Confluence

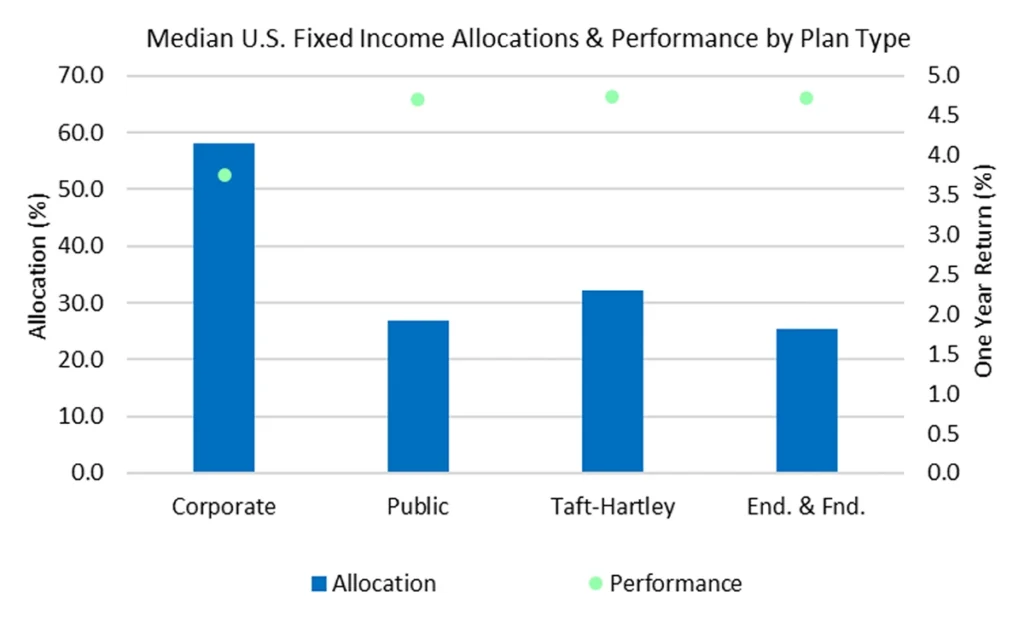

U.S. fixed income performance

The median return for U.S. Fixed Income across all DB plans was 4.43% for the year ending March, compared to 4.35% for the Bloomberg Barclays U.S. Aggregate Index. Despite a decrease of 2%, Corporate plans maintain the highest allocation to U.S. Fixed Income at 58.2%.

Source: Confluence

Source: Confluence

Alternatives performance

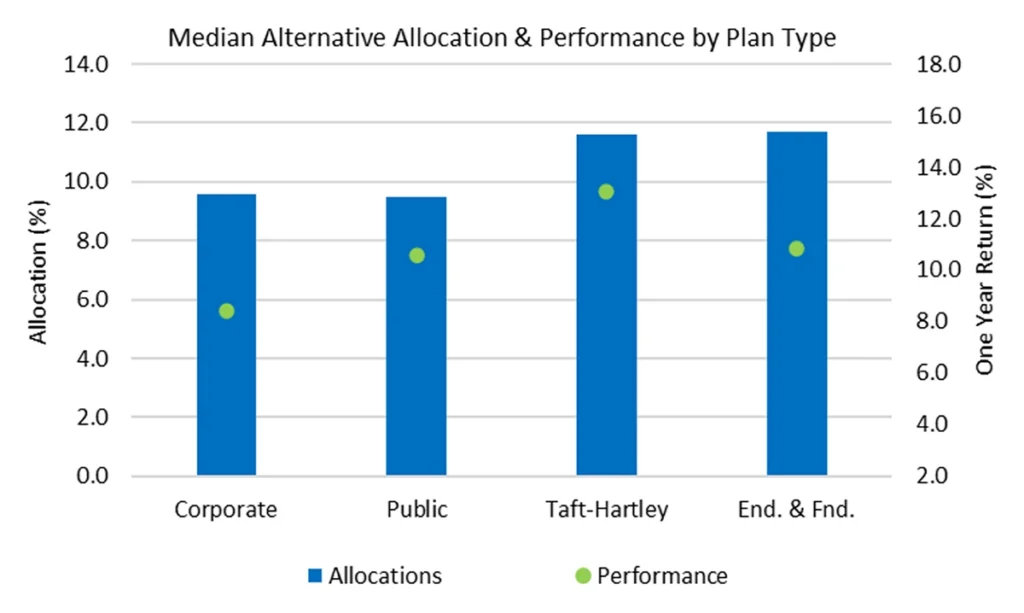

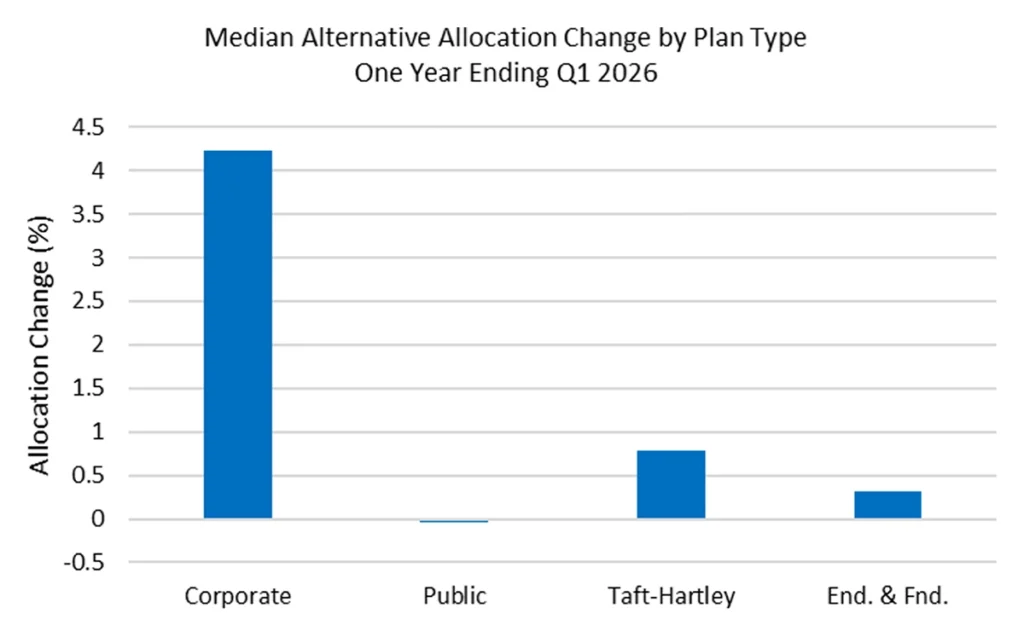

Corporate plans median allocation to alternatives increased by 4.2% to 9.6% in the last year, bringing them closer to the median allocation for all DB plans of 10.15%. Despite the increase they comparatively remain underweight. Endowments & Foundations continue to have the highest median allocation to alternatives at 11.7%.

Source: Confluence

Source: Confluence

Confluence Plan Universe

Confluence Plan Universe is the industry’s most granular analytics tool for plan sponsors including standard and custom peer group comparisons of performance, risk, and asset allocations by plan type and size. The data is sourced directly from over 4,000 institutions using our reporting and analytics solutions, including investment consultants, advisors, and asset owners. Plan Universe is updated quarterly and typically available on or near the following schedule: preliminary data available on the 14th business day after quarter end, a second cut on the 21st business day, and final cut on the 29th business day. The data includes 20+ years’ history on:

- Trust Funds, Corporates, Public Plans, Taft-Hartley, Endowments & Foundations, High Net Worth, Health & Welfare, and custom groups.

- Asset Allocations broken into equity (US, global, global ex-US), fixed income (US, global, and global ex-US), alternatives, real estate (public and private), multi-asset and cash. Emerging Markets allocations are available for equities and debt securities.

- Net and gross performances displayed by quartile with full percentiles via download.

- With all information aggregated by Plan Size.

Disclaimer

The content provided by Confluence Technologies, Inc. is for general informational purposes only and does not constitute legal, regulatory, financial, investment, or other professional advice. It should not be relied upon as a substitute for specific advice tailored to particular circumstances. Recipients should seek guidance from appropriately qualified professionals before making any decisions based on this content.

Unless otherwise stated, Confluence Technologies, Inc. (or the relevant group entity) owns the copyright and all related intellectual property rights in this material, including but not limited to database rights, trademarks, registered trademarks, service marks, and logos.

No part of this content may be adapted, modified, reproduced, republished, uploaded, posted, broadcast, or transmitted to third parties for commercial purposes without prior written consent.

Author

About Confluence® Technologies

Confluence is a global leader in enterprise data and software solutions for regulatory, analytics, and investor communications. Our best-of-breed solutions make it easy and fast to create, share, and operationalize mission-critical reporting and actionable insights essential to the investment management industry. Trusted for over 30 years by the largest asset service providers, asset managers, asset owners, and investment consultants worldwide, our global team of regulatory and analytics experts delivers forward-looking innovations and market-leading solutions, adding efficiency, speed, and accuracy to everything we do. Headquartered in Pittsburgh, PA, with 700+ employees across North America, the United Kingdom, Europe, South Africa, and Australia, Confluence services over 1,000 clients in more than 40 countries. For more information, visit www.confluence.com.